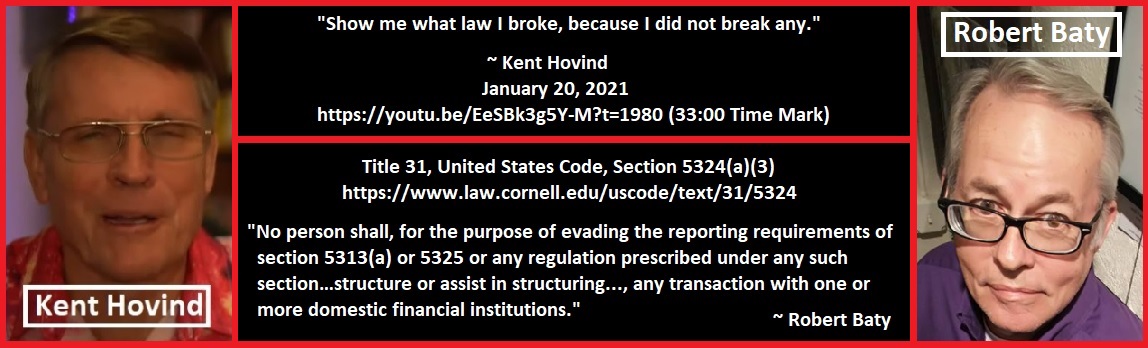

Some of Kent’s people have wondered why I don’t debate Joe Banister.

Bwahahahahahaha!

Joe doesn’t have anything; he, like Kent, lost his tax case!

Kent, come on out. I’ll debate you!

See:

(excerpts)

Tax Roundup, 11/30/16: If at first you don’t succeed, fail, fail again.

November 30th, 2016 by Joe Kristan

That went well. Tax protest figure Joe Banister had a bad day in Tax Court last year when the judge upheld deficiencies of $176,000, 75% fraud penalties, and a $25,000 frivolous return penalty. At the time I predicted:

I doubt Mr Banister is done in court. It’s not typical of hard-core “tax honesty” adherents to just pay assessments.

Sure enough, the appeal of Mr. Banister’s 2015 Tax Court defeat came down last week from the Ninth Circuit appellate court. It went no better:

The Tax Court properly upheld the Commissioner’s determination of deficiencies, additions, and penalties for tax years 2003 through 2006. See 26 U.S.C. § 6201 (setting forth assessment authority of the Internal Revenue Service (“IRS”)); id. at §§ 7601-7613 (providing the IRS with broad investigatory powers); Grimes v. Comm’r, 806 F.2d 1451, 1453 (9th Cir. 1986) (restating that tax on income is constitutional and defining taxable income); Bradford v. Comm’r, 796 F.2d 303, 307 (9th Cir. 1986) (affirming the Tax Court’s finding that fraud had been established by clear and convincing evidence based on, inter alia, a failure to file tax returns for four consecutive years).

The Tax Court did not abuse its discretion by imposing a penalty against Banister for taking a frivolous position.

The appeals panel tacked on its own $8,000 frivolity penalty for bothering them: “Sanctions are appropriate when the result of an appeal is obvious and the arguments of error are wholly without merit.”

From his Tax Court case (my emphasis):

During the course of this case, petitioner did not deny receipt of the income determined in the statutory notice and did not identify deductions that had not his cross-examination of respondent’s witnesses at trial have been directed to his claim that the statutory notice was invalid because it was not signed by an authorized person and that, as a result, this Court lacks jurisdiction over his case. In his pretrial memorandum he also asserted that his U.S. income was not subject to tax and that he had no obligation to file tax returns,repeating or restating the arguments that had led to his disqualification to practice before the IRS and his loss of his certified public accountant’s license. Petitioner refused to testify at trial, citing his Fifth Amendment privilege against self-incrimination. Instead he submitted a “motion for offer of proof” that, to the extent intelligible at all, repeated and elaborated on his argument that his U.S. income was not subject to income tax.

(T)he Tax Fairy has yet to emerge from tax protester word clouds.

She didn’t intervene with the appeals court, so unless the U.S. Supreme Court takes the case (not happening), it’s now a matter of collection.

Mr. Banister still seems convinced that his arguments are right.

Taxpayers pondering whether to follow Mr. Banister’s arguments should understand that it doesn’t matter what he thinks when the IRS, the Tax Court, and the federal appeals courts think otherwise.

Comments

Hovind Hero Loses in Court – Joe Banister! — No Comments

HTML tags allowed in your comment: <a href="" title=""> <abbr title=""> <acronym title=""> <b> <blockquote cite=""> <cite> <code> <del datetime=""> <em> <i> <q cite=""> <s> <strike> <strong>